PETALING JAYA: There could be potential mergers and acquisitions arising from Sime Darby Bhd's five-year strategy blueprint, according to research analysts.

In a note issued yesterday, OSK Research pointed out that the conglomerate's management had guided for capital expenditure of RM6bil in the current financial year (FY12) which included an allowance for potential mergers and acquisitions.

This may start to take shape during the five-year period and can possibly involve a tie-up with Felda Global Ventures, which owns significant downstream assets outside Malaysia.

Sime Darby president and group chief executive Datuk Mohd Bakke Salleh, formerly Felda's chief, has intimate knowledge of these assets, which will help in establishing strategic tie-ups.”

CIMB Research concurred, saying in a note that Sime Darby's management spoke about landbank expansion for its plantation division, broadening of its industrial business through the potential acquisition of the Bucyrus dealership in Australia's Northern Territory from Caterpillar, and a bigger presence for its motor division in the Asia-Pacific during a recent briefing.

“Sime Darby should have no problem funding mergers and acquisitions in view of its low gearing of 8.7 times,” said CIMB Research.

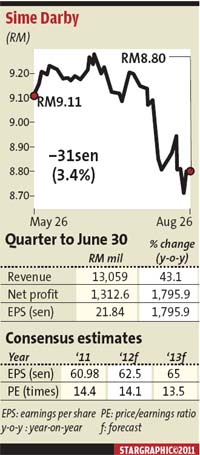

Meanwhile, research analysts are bullish on the Sime Darby stock after the conglomerate posted record-breaking results for the financial year ended June 30, (FY11).

Analysts said Sime Darby's financial results were above expectations, and pointed out that its plantation, industrial and motor divisions should continue to drive growth in the near future.

On Thursday, Sime Darby posted a 404% year-on-year (y-o-y) jump in net profit to RM3.66bil and a 28.8% year-on-year increase in revenue to RM41.86bil for FY11.

The plantation division was the top earnings contributor with a 56% y-o-y increase in profit before interest and tax (PBIT)) to RM3.3bil, followed by the industrial division which recorded its highest ever PBIT with a 41% y-o-y increase to RM1.1bil, and the motor division which registered a 64% y-o-y increase in PBIT to RM633mil.

The motor division was the highest revenue contributor to the group for the first time ever with RM14.85bil, followed by the plantation division with RM13.17bil.

OSK Research upgraded Sime Darby's stock from “sell” to “neutral,” with a fair value of RM9.21.

In a note issued yesterday, ECM Libra Investment Research upgraded the stock of Sime Darby to a “trading buy” from “hold”, with a target price of RM10.95.

ECM Libra Investment Research head Bernard Ching stated that for FY11, the industrial division was driven by strong Caterpillar equipment sales in Australia as well as China while the motor division continued to see strong BMW sales in China and Malaysia.

On the outlook for FY12, Ching said the plantation division was expected to see a 5% to 6% fresh fruit bunches (FFB) production growth as the industry comes out of the biological down cycle.

Ching added that the industrial division could surprise again as Caterpillar had recently acquired Bucyrus International.

Kenanga Research also maintained a “outperform” call on Sime Darby's stock although its target price was lowered to RM9.70 from RM11.06, mainly due to the analyst's negative outlook on CPO prices.

“Our 13.5x forward PE (price to earnings) is in line with expected forward PE for Kuala Lumpur Plantation Index when CPO prices reach the RM2,900 level.” |