As for price, the most recent fabrication yard transaction was between Ramunia Holdings Bhd and OilFab Sdn Bhd. The price paid for the yard was RM1.47 million per acre. Assuming a similar price is used to purchase Sime’s Pasir Gudang yard, it would amount to RM482 million which

MMHE can pay for with cash raised from its IPO (current net cash is RM1.7 billion).

We believe this transaction could materialise. The most synergistic to MMHE would be to acquire Sime’s Pasir Gudang yard given the proximity to its yard.

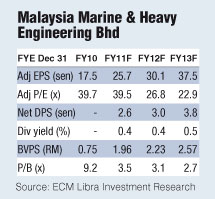

With this M&A news coming into play and also the potential for MMHE to announce a new major contract in Turkmenistan (potentially more than RM4 billion), we view that MMHE, despite current expensive valuations, will hold up in the coming months and as such we stay put with our “hold” call and raise valuations.

We are raising our price-earnings ratio on the group to 25 times from 20 times. The rationale for the 25 times multiple is from mirroring Kencana Petroleum Bhd’s peak of more than 25 times that was seen during the 2007 O&G run. With a 25 times PER pegging CY11 earnings per share our target price of RM5.80 is raised to RM7.25. We make no changes to estimates at this juncture.

We will be writing further at a later date on potential earnings accretion to MMHE. — ECM Libra Research |