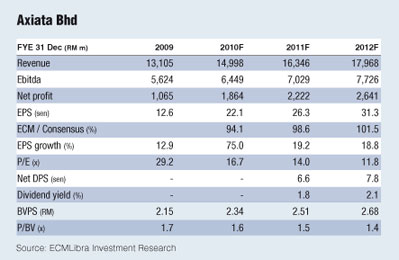

Maintain buy at RM3.69 with revised target price of RM4.50 (from RM4.15): Axiata’s 3MFY10 revenue was in line while core net profit was above house and consensus estimates. Reported net profit was much higher as Axiata recorded an exceptional gain from the partial disposal of XL stake. Revenue and net profit growth was driven by strong year-on-year (y-o-y) performance by all major operating units, including Dialog.

Celcom and XL experienced strong double-digit growth both in terms of revenue and profitability on the back of steady subs growth and ever improving earnings before interest, tax, depreciation and amortisation (Ebitda) margins. Both companies’ Ebitda margins are near record highs at 45.4% and 51% respectively. But management is guiding for Ebitda margin to stabilise at mid-40s level due to competition.

Dialog surprisingly posted a net profit of Sri Lankan rupee (SLR) 705 million (RM20.19 million) compared to a loss of SLR1.87 billion in 3MFY09. The turnaround was mainly due to a 20-percentage point rise in Ebitda margin y-o-y to 34% due to opex improvements. Meanwhile, Robi managed to continue churning out profits albeit lower q-o-q despite being more aggressive in acquiring subs.

Prospects look positive for the group as a whole, mainly driven by Celcom and XL while previously underperforming opcos (Dialog and Robi) return to the black. High single-digit growth from Celcom and high teens growth from XL will underpin earnings growth. Despite volatile earnings, Robi has  remained profitable for a second consecutive quarter and looks to be on track to remain profitable throughout the year. A positive surprise is Dialog’s turnaround, and we are hopeful that continued cost control should enable Dialog to stay in the black this year. remained profitable for a second consecutive quarter and looks to be on track to remain profitable throughout the year. A positive surprise is Dialog’s turnaround, and we are hopeful that continued cost control should enable Dialog to stay in the black this year.

We maintain our earnings estimates as competition will likely put downward pressure on the good margins recorded in 1QFY10 while contribution from XL will be lower from 2QFY10 onwards as Axiata trimmed its stake in XL from 86.49% to 68.49% in March. We also expect financing costs to increase given the recent US$300 million (RM978 million) bonds issuance.

However, we revised our sum-of-parts target price higher to RM4.50 (previously RM4.15) due to lower net debt due to the RM1.7 billion cash received from the partial disposal of XL stake. Hence, we reiterate our buy call. — ECM Libra Investment Research, May 31 |