Maintain buy at RM2.14 with higher target price of RM2.68: Media Prima Bhd (MP) is due to release its 1QFY10 results on May 18. We understand that MP will record 1Q net profit of circa RM20 million. This is a marked improvement from the 1QFY09 core net loss of RM9.9 million. Not only did 1Q TV advertising expenditure (adex) grow by double digits year-on-year, it grew by high single digits vis-à-vis a robust 1QFY08 (buoyed by the 12th general election then). The New Straits Times Press (NSTP) will also commence contributing to earnings in 1QFY10. We estimate that NSTP contributed circa RM10 million to MP’s net profit in 1QFY10.

In tandem with healthy consumer sentiment (two-year high) driven by the recovering economy, total adex sentiment and growth have improved markedly. We understand that TV booking cycles have improved from two weeks to slightly over a month. Recall that TV booking cycles were approximately three months during the “heady” 2007 to 1H08 period. Therefore, despite potentially posting good 1Q10 results, there is a lot of room for improvement at MP.

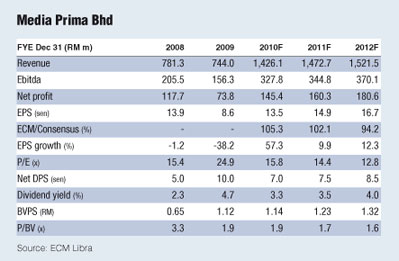

We now assume 7.5% TV adex growth or 1.5 times real GDP growth for FY10 and 5% TV adex growth or one time real GDP growth thereafter (6% TV adex growth per annum previously). This is moderated by lower daily circulation of Berita Harian and New Straits Times as per the recent Audit Bureau Of Circulation 2009 Audit Report. The net impact is to leave our FY10 earnings estimates relatively unchanged but our FY11 and FY12 earnings estimates trimmed by 11% and 13% respectively.

We now ascribe a one-year forward PE of 18 times (average since listing in October 2003) to arrive at a revised target price of RM2.68 (RM2.17 previously on 13 times one-year forward PE).

Recall that MP was trading at 17 times to 21 times one-year forward PE during the 2007 to 1H08 period. Now that consumer and thus, adex sentiment has recovered to the levels witnessed during that period, we believe that MP should trade at those valuations.

Anyhow, as earnings are on the mend, MP should be trading close to historical average valuations anyway. We maintain our buy call on MP. It remains our top pick in the media sector for 25% upside potential. We will upgrade our estimates and target price should adex grow stronger than expected.

|