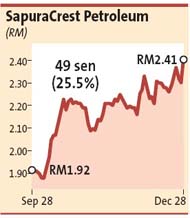

PETALING JAYA: Analysts are generally bullish over SapuraCrest Petroleum Bhd’s prospects, seeing that it had recently won several major contracts worth billions against other established competitors and was expected to secure more contracts in future.

In a filing on Dec 24 to Bursa Malaysia the company said its wholly owned subsidiary TLO Offshore Sdn Bhd had been awarded a joint contract by 11 Petronas’ production sharing contractors (PSCs) for provision of works and services related to transportation and installation of offshore oil and gas facilities and PSC structures from 2010 to 2012 .

An analyst with Kenanga Research said the confirmed PSC works are for three years – from 2010 to 2012 – with options for two further extensions of one year each.

“The scope of works and the project schedule will be specified and determined on a yearly basis. The price for the confirmed scope of works for 2010 is about RM1.5bil and some of the projects are exepcted to start in March,” he said.

The analyst said the contracts could be worth more as, extrapolating the RM1.5bil for 2010, the ongoing projects could amount to RM4.5bil.

”For now, we have kept our expectations status quo. However, we will not be surprise should the contract total over RM3bil,” the analyst said.

He added: “We look forward to the company’s third quarter financial results ending Oct 31 later this week which could have some upside surprises.”

On the impact of the awards, he said the contracts would not have any material effect on the issued and paid-up capital of the company.

“But we expect the contracts to contribute positively to the company’s earnings and net tangible assets for the financial year ending Jan 31, 2011 (FY2011) and the financial periods thereafter over the contract period.”

SapuraCrest’s order book had ballooned to RM8.5bil after TL Offshore secured four out of five packages in the Petronas umbrella tender.

Kenanga Research has a “hold” call on the stock and a target price of RM2.49.

An analyst with ECMLibra Investment Research said the research house had been very conservative with SapuraCrest Petroleum’s forward estimates for FY11 onwards, projecting previously a decline in earninsg per share of 8.6% from FY10.

“This was mainly due to the uncertainty of the timing of these contracts. However, with this long awaited contracts now confirmed and coming into fruition, we have raisied our estimates accordingly,” he said.

The analyst said judging from previous transport and installation jobs, the research house viewed it possible for the company to achieve up to 10% margin at earnings before interest and tax level.

“However, should the job require third party charter of vessels to complete jobs, we believe margins then would be closer to 5% range. Hence, we are imputing the latter margin in our revised estimates for now,” he noted.

The analyst said the research house raised its FY2011 and FY2012 estimates by 34% and 34.1% respectively, while FY2010 was left unchanged.

ECMLibra Investment Research raised its target price to RM2.16 from RM1.55 after news of the contracts secured by the company.

“We continue to have a hold call on the company and view the news as already been factored into the stock,” he said, adding that a meeting with management was due to get more details on the contracts and to confirm margin estimates. |