ECM Libra Research has maintained its buy call on Genting Malaysia Bhd (GenM) at RM2.78 with an unchanged target price of RM3.08, as the research house believed there would be minimal impact from the subscription of US$15 million (RM50.8 million) mortgage notes issued by Wynn Resorts Ltd on GenM’s forward earnings per share (EPS).

In a research report yesterday, it said GenM’s forward EPS would only be impacted at 0.2 sen or 1%. “While GenM is taking steps to enhance returns on its cash hoard, we note that its subscription of Wynn Resorts’ notes only represented about 1% of RM5.13 billion cash hoard,” it added.

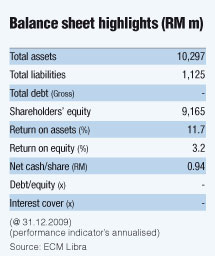

ECM Libra said assuming a yield of 8% on the notes, GenM’s portion of the notes would generate interest income of RM13.5 million (about 1.1% of its financial year ending Dec 31, 2010 net profit).

“The lower yields reflected improved investor sentiment, as the gaming industry, particularly in Macau is improving,” the research house explained.

GenM announced on Wednesday that it had completed the subscription to the notes, which had an aggregate principal amount of US$500 million. The notes were issued at a discount of 97.823% par, which carries an interest of 7.875% and is due in 2017.

ECM Libra said the subscription of notes followed GenM and its holding company GENTING BHD [ registerQuotes("GENTING", "GENTING_span"); ]’s subscription of senior secured notes in MGM Mirage in May this year. GenM and Genting Bhd had each subscribed for US$50 million of the US$1.5 billion aggregate principal amount of MGM’s notes, which had higher yields in excess of 10%.

|

|

RHB Research said the subscription seemed to be GenM’s way of putting its cash reserves to “good use”, given the decent rate of return and high yield of above 8% for the notes.

Nevertheless, just like its subscription of MGM bonds in May, it would not give GenM any access to Wynn’s gaming earnings, unless there was a default in notes, which would enable GenM to get a small share of all of Wynn’s assets (which includes the 380-table Wynn Resorts in Macau).

“We believe this investment also indicates that GenM may still be far from finding any regional expansion opportunities, especially as regional gaming asset valuations have risen significantly of late,” it said.

However, RHB said although an earnings-accretive and EPS-enhancing acquisition of a regional gaming asset would be able to generate more excitement for the stock in the medium term than an investment like this, it conceded that this was still better than no investment at all as the alternative would mean GenM would only earn low fixed deposit rates on its RM5.13 billion cash pile.

RHB Research maintained its market perform call with an unchanged fair value of RM3, given expectations that investor sentiment would be weak in the near term, as a result of the potential cannibalisation of earnings when the Singaporean integrated resorts open.

“This, in addition to investor disappointment that no capital management in the form of special dividends or treasury share cancellation seems to be forthcoming,” it said.

The research house said this was despite GenM’s seeming difficulty in finding an overseas gaming venture to invest in, which would provide them with their target return of investment of 15% to 20%.

Yesterday, GenM gained two sen to close at RM2.80.

|