|

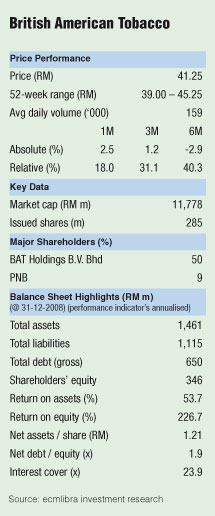

ECM Libra Research has reiterated its hold call on British American Tobacco (BAT) and maintained its target price at RM37, saying the company’s results for the third quarter (3Q) ended Sept 30, 2008 were within its expectations.

“We are maintaining our forecasts and discounted cash flow-derived target price of RM37 at this juncture, despite earnings coming in marginally above our forecasts, due to a damaging mix of higher priced cigarettes and worsening economic outlook,” it said in a recent note.

The research house said BAT’s revenue and net profit for the nine months of FY08 made up 77% and 81% of its full-year estimates respectively.

“Net profit margins continued to improve sequentially to 21.2% compared with 19.3% in 2Q08. The improvements came on the back of higher pricing following the 20% increase in excise tax in September, where BAT had increased its cigarette prices by a bigger quantum than the tax hike,” it said.

It also noted that, year-on-year, revenue and earnings were up 8.9% and 13.4% respectively, owing to reduced competitive price discounting, continued productivity savings and lower financing costs.

ECM Libra said BAT’s performance boost came even as total industry volume (TIV) declined by 2.2% for the nine months of 2008. BAT outperformed the industry by registering a decline of only 1.5%, driven by the strong performance of its Dunhill and Pall Mall brands.

Both brands increased their market share in the premium category (Dunhill with 41.4% market share) and value-for-money category (Pall Mall with 8.2% market share).

BAT declared a second interim dividend of 76 sen per share, tax exempt, which brings total dividend payout for FY08 to RM1.89 per share, or 69% of the forecast payout.

The research house said it expected a final dividend payment of 86 sen for 4Q08, which would bring BAT’s gross dividend yield for FY08 to 6.7%, assuming 100% payout ratio.

“We reiterate our hold rating for BAT due to its high dividend yield and strong brand portfolio,” it said, adding the risks to its recommendation included lower than expected total industry volume (TIV).

BAT surged 75 sen to close at RM42 last Friday.

|