Boustead Holdings Bhd (Aug 16, RM4.30)

Maintain buy at RM4.36 with target price of RM4.48: Last Friday, Boustead Holdings subsidiary Boustead Heavy Industries Corp (BHIC) announced the receipt of the letter of award from the government for the contract to undertake In Service Support (ISS) for the two Royal Malaysian Navy’s Prime Minister Class Scorpene Submarines. The contract is worth a total of €193 million (RM772 million) and RM532 million and is effective till Nov 30, 2015. The job will be carried out by Boustead DCNS Naval Corp, a JV between DCNS (40%) and BHIC (60%). Note that the contract sum differs slightly from the RM600 million that was originally announced in June 2009, as it includes other service components.

This is welcome news for the group considering that it has been more than a year since the letter of intent was received. In terms of earnings contribution, we have been guided that the first few years’ contribution will be lower given that the submarines are still relatively new and will not require much service. As such, we expect this contract to contribute more significantly from 2012 or 2013 onwards.

We make no changes to our estimates with the inclusion of this job as we view that we have captured it in our forward earnings for BHIC. To note, margin expectation from the jobs is in the 5% to 10% range at earnings before interest and tax level.

Boustead is carrying out the job on a JV basis in order to get technology transfer from DCNS SA, the supplier of the twoScorpene submarines to the Royal Malaysian Navy. Judging from recent share price movement, there could be more in store for Boustead in the coming months. To recap, this is  the second job that has been firmed up with the government so far this year. The first was the RM130 million order of fast interceptor craft in June. Therefore, we believe that the group could be closer to being awarded another six vessels to build for the navy soon, given that the sixth and final patrol vessel from the previous contract is to be delivered this month. The contract is expected to be sizeable, with each vessel costing up to RM1 billion, and will likely lead us to adjust our estimates upwards. the second job that has been firmed up with the government so far this year. The first was the RM130 million order of fast interceptor craft in June. Therefore, we believe that the group could be closer to being awarded another six vessels to build for the navy soon, given that the sixth and final patrol vessel from the previous contract is to be delivered this month. The contract is expected to be sizeable, with each vessel costing up to RM1 billion, and will likely lead us to adjust our estimates upwards.

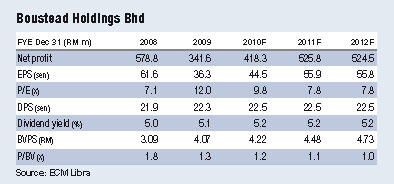

We maintain our buy call on Boustead Holdings for now with a RM4.48 target price (eight times historical PER pegging FY2011 EPS) in the interim despite Boustead trading close to our target price. We will be reviewing this when 2QFY2010 results are announced at the end of the month. — ECM Libra Investment Research

|