Sunway Holdings Bhd

(June 18, RM1.53)

Reiterate buy at RM1.53 with target price of RM2: Sunway announced last Thursday that they have entered into a memorandum of understanding (MoU) with Dasa Tourist to explore the possibility of forming a joint venture to construct and develop a 34 storey building comprising 71 commercial units and 176 residential units in Colombo city, Sri Lanka.

The proposed development is located on prime freehold land in the premium mixed-used zone of Bambalapitiya in District Colombo 4 with a potential to generate a total sellable area of 400,000 sq ft. Total gross development value (GDV) is estimated to be RM250 million. Sunway will undertake feasibility studies and market research within two months from the date of the MoU.

Colombo city is the trade capital of Sri Lanka and is located within the most highly populated Western Province. With political turmoil behind them, Sri Lanka has since experienced economic growth, with GDP rising 6.2% in the three months ended December 2009 from a year earlier after gaining 4.2% in the previous quarter. Colombo city is the trade capital of Sri Lanka and is located within the most highly populated Western Province. With political turmoil behind them, Sri Lanka has since experienced economic growth, with GDP rising 6.2% in the three months ended December 2009 from a year earlier after gaining 4.2% in the previous quarter.

Inflation remains low while the repurchase rate and reverse repurchase rate was maintained at 7.5% and 9.75% respectively, a five-year low. With US$1 billion (RM3.25 billion) pledged in infrastructure spending, the economy is headed for a boost while many multinational corporations have stepped up operations and investments.

While we acknowledge the risks involved in venturing into unchartered waters, the materialisation of this project would allow Sunway to test the Sri Lankan market on a smaller scale, in comparison with its other property development ventures abroad.

We are positive on this development as it offers an opportunity for geographical expansion as the group does not currently have a presence in Sri Lanka.

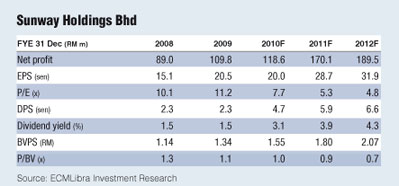

Sunway is our top buy for the construction sector. This is premised on (1) strong earnings growth of 46.4% in FY10, (2) undemanding forward P/E valuation of 7.7 times, (3) more land bank acquisition in the pipeline, and (4) strength in securing overseas construction contracts, in particular Abu Dhabi and India.

Our target price is unchanged at RM2 which is derived from 10 times P/E on FY10 EPS. This is further supported by sum-of-parts valuation of RM2.74. — ECM Libra Research, June 18

|