Lots of potential but uncertain in near term. Earnings visibility still in doubt

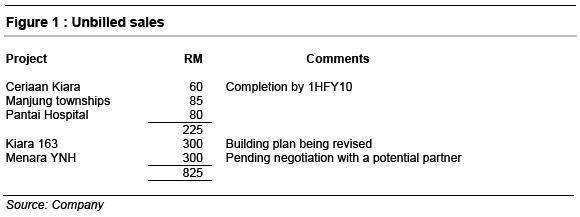

Following a post-1QFY2010 results briefing last week, we gathered further information from the management. Although earnings visibility for FY2010 exceeds our earlier expectation as a result of better than expected sales of completed inventories, we are still concern about earnings visibility from FY2011 onwards. Unbilled sales as at 1QFY2010 were RM825 million.

However, stripping away unbilled sales of Kiara 163 (RM300 million) and retail portion of Menara YNH (RM300 million) which are still subject to uncertainty, adjusted unbilled sales only amount to RM225 million which is less than one year revenue.

Ceriaan Kiara will cease contribution by 1HFY2010

Much of the company’s 1QFY2010 earnings have been contributed by Ceriaan Kiara, the company’s maiden condominium project in Mont’Kiara. However, physical construction of this project has been substantially completed and will be handed-over to purchasers by 1HFY2010. As such, there will not be further contribution in 2HFY10. We have however underestimated the sales of unsold inventories. We understand that there are about 60 unsold units and the company has so far managed to sell 15 units in April alone for about RM440 psf or about RM1 million per unit.

Fraser Residence will be launched in June

Management has informed that the sub-structure works for Fraser Residence project behind Renaissance Hotel has already been tendered out and sales preview is targeted in June 2010. So far, there are 300 registrants for this project with 446 units and GDV of RM550 million.

Similar to Fraser Place, this project will be managed by Fraser Hospitality of Singapore. All units will be sold on fully furnished basis and YNH will provide a five-year rental guarantee.

Kiara 163 subject to building plan revision

YNH has previously sold RM300 million worth of retail and office space in this mixed commercial and serviced apartment project in Mont’Kiara which has a GDV of RM875 million. Although management has tendered out the sub-structure works, the building plan is still being reviewed by anchor tenant. Upon revision of the building plan, YNH will need to procure the advertising permit before the serviced apartments can be launched. This project which was initially slated for launch in 2008 has not been delayed for two years.

Looking for new partners for Menara YNH

Following the failed partnership with CapitaLand and the aborted sale to Kuwait Finance House, YNH is now talking to a potential foreign investor which will buy the building as well as take a 20%-30% equity stake in the development project. Management has guided that an announcement will be made once a definitive agreement is signed. Although the company has already sold the retail podium for RM300 million, we believe construction is not about to start anytime soon pending the negotiation with the potential new partner.

Potential entry of foreign investors in Genting project

YNH also alluded to the potential entry of a consortium of foreign investors to jointly develop the Genting project into a luxury hillside resort. The consortium may take up a 50% stake in the project. Notwithstanding a low entry cost of just RM3.90 psf versus infrastructure cost of RM10 psf incurred by previous landowner, we are hard pressed to be bullish of this project due to difficulty in assessing the fundamental demand for such properties.

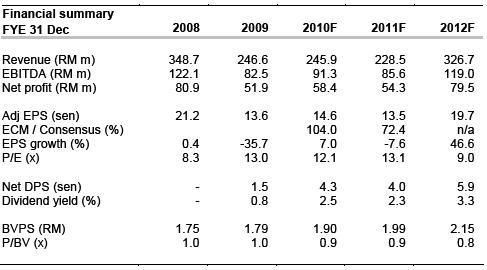

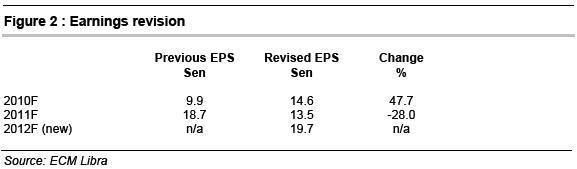

Earnings revision

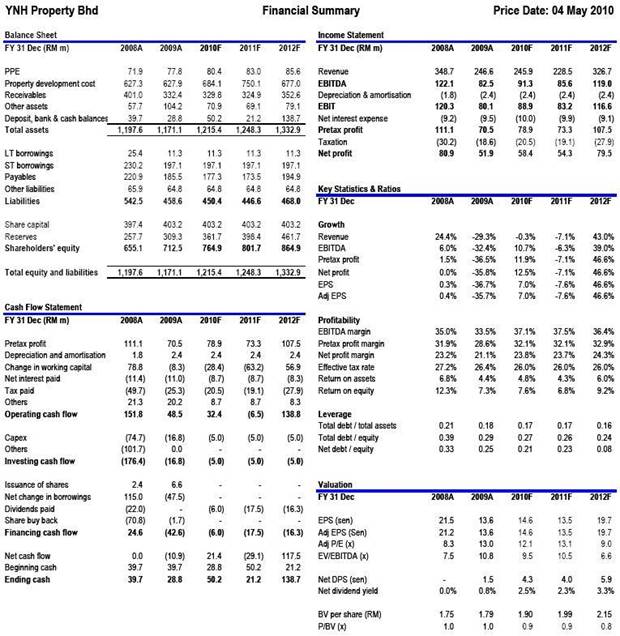

We have revised our earnings estimate for FY2010 (+47.7%) and FY2011 (-28.0%) as well as introduce FY2012 numbers. Our revision has taken into account (1) higher than expected sale of inventory in FY2010; and (2) launching of Fraser Residence in June 2010. We did not take into account any earnings from Kiara 163 and Menara YNH due to on-going review of building plan and negotiation with investors respectively, as there is considerable risk of further delay in construction start.

Maintain SELL

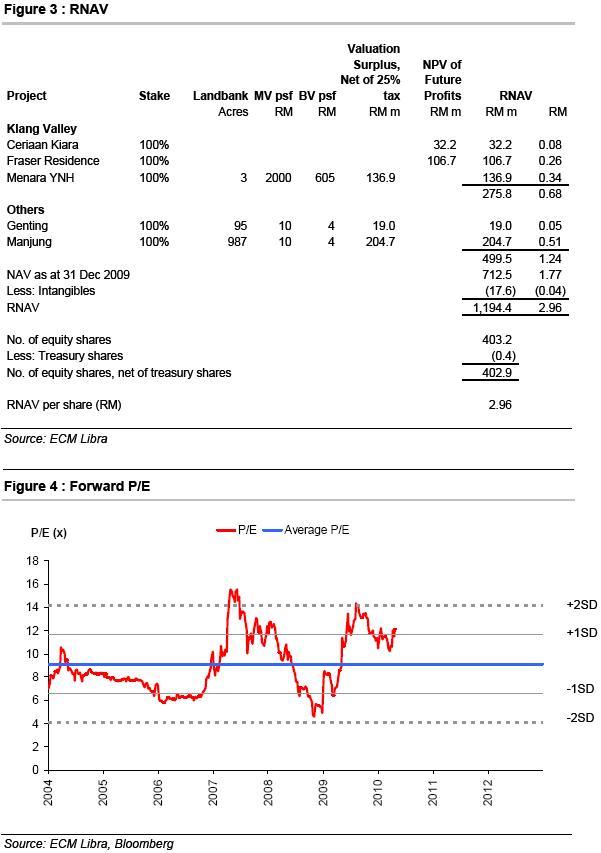

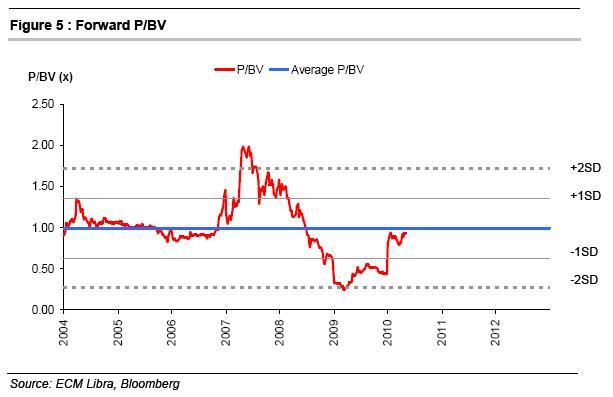

We reiterate our sell call as we continued to be concern of YNH earnings visibility as planned projects face risks of further delay. Although the stock is trading at steep discount to RNAV of RM2.96 (previously RM3.14), valuation gap is unlikely to narrow anytime soon given risk of further project delay. Furthermore, when the new accounting standard IFRIC 15 is being implemented from FY2011, YNH may even record accounting loss until Fraser Residence is completed in FY2013 or FY2014. This will further dampen investors’ confidence in the stock. Our target price which continued to be pegged to 10x of average FY2010 and FY2011 EPS has been revised from RM1.43 to RM1.40. We believe our target price is fair as it would trade closer to average P/E of 9.1x as compared to current P/E of 12.1x which is higher than 1x standard deviation above the average P/E in the past. At current valuation, YNH is more expensive than Sunrise, one of our top picks for the property sector.

|