ANALYSTS have kept their recommendations for the Malaysian telecommunication sector following the release of Maxis Bhd’s draft initial public offering (IPO) prospectus.

The company is expected to be relisted by the end of this year.

OSK Research has not budged from its neutral stance for the sector, given unattractive valuations and intense competition among telco players.

According to the research house, at a price-to-earnings ratio (PER) of 17.2 times, the sector is deemed more expensive compared to the regional average of 16.5 times. The regional figure includes sector valuations in Malaysia, Singapore and Indonesia.

The 17.2 times PER is also deemed less attractive than the Malaysian stock exchange’s 2010 PE estimates of 16 times.

OSK Research also foresees more rivalry in the Malaysian industry with the entry of the country’s latest mobile virtual network operator Tune Talk Sdn Bhd which is offering below-market prepaid rates.

“(The neutral call is also based on) the structural deceleration in growth as domestic mobile  penetration has exceeded parity,” it said in a note yesterday. penetration has exceeded parity,” it said in a note yesterday.

The relisting of Maxis would negatively impact its rivals DIGI.COM BHD [ registerQuotes("DIGI", "DIGI_span"); ] and TELEKOM MALAYSIA BHD [ registerQuotes("TM", "TM_span"); ] (TM), added OSK Research.

“We believe the relisting of Maxis will be negative for DiGi given its smaller share liquidity and market capitalisation, and Maxis’ relatively more superior Ebitda (earnings before interest, taxes, depreciation, and amortisation) margin, and dividend payout potential.

“We believe TM could also be indirectly impacted by virtue of Maxis being pitted as a dividend play and therefore likely to be able to demonstrate a more sustainable and certain dividend payout going forward,” said the research house.

Maxis is, however, not expected to directly compete against Axiata, because Maxis will be refloated without its foreign operations.

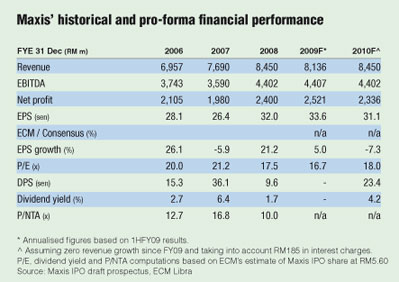

Meanwhile, ECM Libra Research expects Maxis’ IPO to be priced between RM5 and RM6.20 a share, assuming a PER of between 16 times and 20 times financial year ending December 2010’s earnings.

The most likely estimate is RM5.60 based on a PER of 18 times for Maxis by virtue of the  firm’s mobile market leadership over DiGi and discount to TM’s fixed-line and broadband monopoly. At RM5.60, Maxis is expected to generate a minimum dividend yield of 4.2% in FY10, it said. firm’s mobile market leadership over DiGi and discount to TM’s fixed-line and broadband monopoly. At RM5.60, Maxis is expected to generate a minimum dividend yield of 4.2% in FY10, it said.

“Such yields are lower than our estimates for DiGi and TM, but perhaps investors may overlook this to have a stake in a blue-chip company that may fetch a market capitalisation of RM42 billion,” said ECM Research which maintained its overweight call on the local telco sector.

Maxis’ IPO involves an offer for sale of 2.25 billion shares or 30% of the firm’s issued share capital of 7.5 billion shares.

The 2.25 billion shares comprise 2.08 billion shares for institutional investors, and 174.8 million units for the Malaysian public or 27.67% and 2.33% respectively, of total issued share capital.

|